China’s Rare Earth Controls: What It Means for the US

The U.S.–China trade war is an ongoing conflict marked by tariffs and export controls between the world’s two largest economies. Both nations have targeted goods, including rare earth minerals vital for technology and defense. The dispute has unsettled global supply chain management, forcing companies to rethink their sourcing strategies. Despite temporary pauses, the conflict remains unresolved.

The latest round of US–China trade tensions revolves around an increasingly strategic commodity: rare earth minerals. The escalation began earlier this year when President Donald Trump raised tariffs on a broad range of Chinese goods, pushing significant rates on some imports. Beijing responded in April by tightening export controls on seven key rare-earth elements and related magnet materials, prized for their supplier quality.

The standoff intensified again in early October. China announced a second, wider set of restrictions, this time extending beyond raw minerals to include an additional five rare-earth elements, specialized production technology, and equipment critical to global manufacturing of permanent magnets.

Beijing also introduced a new rule requiring foreign companies to obtain licenses for any product exported from China that contains even trace amounts of controlled rare earths. These measures signaled a shift from targeted limits to a far more sweeping export-control regime designed to give China leverage over downstream supply chains.

Washington’s reaction came swiftly. Citing China’s tightening grip on critical minerals and their economic value, Trump said the US would impose a fresh 100% tariff on Chinese imports beginning November 1 and would move to restrict certain U.S. software exports. The announcement revived a trade dispute that had briefly cooled during a tariff “pause” negotiated earlier in the year.

(Also read: Trump’s Tariffs: What Will Happen This 2025?)

The strategic value of rare earths

Rare earth minerals, a group of 17 metallic elements, are far more common than their name suggests. Found throughout the Earth’s crust, these materials are more abundant than gold—but extracting and refining them is complex, costly, and environmentally taxing.

Despite the challenges, rare earths are indispensable to modern life. These power everyday electronics like smartphones and LED lights, and are critical for technologies under the renewable energy market, including wind turbines and EV batteries. Their unique chemical properties make them essential in a range of high-tech applications that are increasingly central to sustainability and the global economy.

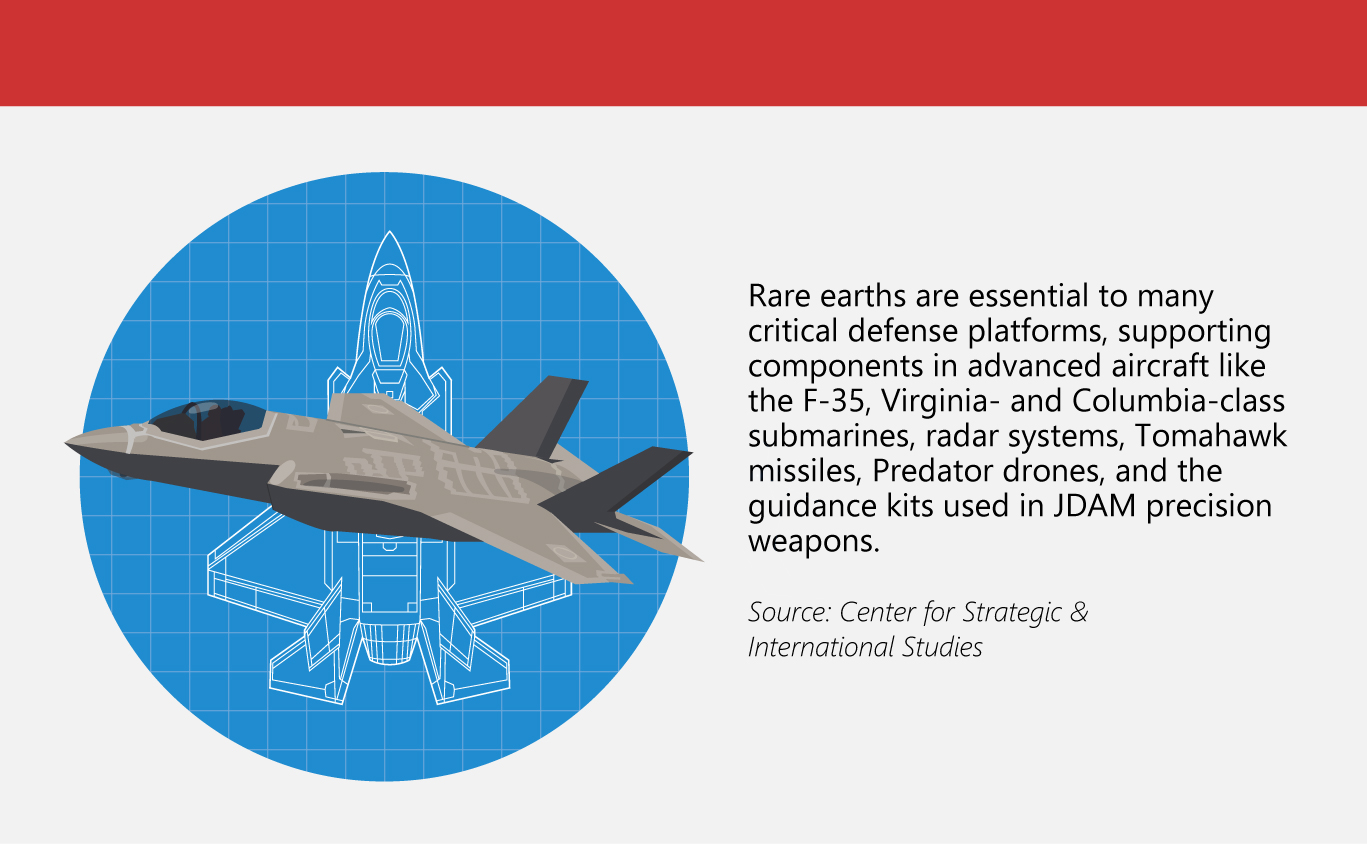

Beyond consumer technology, rare earths are vital for medical electronics and defense applications. They are used in MRI scanners and cancer treatment equipment, and form key components in military systems, including fighter jets, lasers, and satellites. In short, these seemingly obscure metals underpin everything from electronics manufacturing to national security.

China dominates the global rare earths market, both as a producer and consumer. In 2024, the country’s rare earth reserves were estimated at roughly 44 million tonnes, giving it a significant edge over other nations. Its dominance extends beyond rare earths: China is also the leading player in other critical minerals, controlling nearly 99% of refined gallium production worldwide—a key input for the industrial market.

According to the International Energy Agency (IEA), 61% of mined rare earths originate from China, while the country oversees 92% of the global processing stage. This near-monopoly means China produces more than 90% of the world’s processed rare earths and the magnets derived from them.

These materials’ strategic importance was underscored when U.S. automakers scaled back production due to shortages, illustrating how China can leverage its rare earth supply to influence manufacturing technologies and industries.

Efforts to dilute China’s monopoly

The US lags behind China in producing advanced defense technologies, as Beijing accelerates munitions output and acquires sophisticated weapons systems at a rate five to six times faster than Washington. While China approaches its military buildup with a near-wartime mindset, the US largely remains in peacetime mode.

Even before recent export restrictions, the American defense industrial base struggled with limited capacity and lacked the flexibility to scale production for critical systems. New constraints on rare earths and other strategic minerals risk widening this gap, giving China an advantage in rapidly enhancing its military capabilities.

Efforts to establish a fully domestic rare earth supply chain remain in their infancy. In January 2025, USA Rare Earths produced its first high-purity sample of dysprosium oxide, using ore from the Round Top deposit in Texas and processed at a research facility in Colorado. The company hailed the milestone as a breakthrough for US rare earth production. Yet converting laboratory success into large-scale commercial output capable of reducing reliance on China will take years, keeping the US dependent on foreign sources.

Globally, several nations are investing in both light and heavy rare earth deposits, but China continues to dominate the refined heavy rare earth market. Countries like Australia, Japan, and Vietnam are expanding mining, processing, research, and magnet production to diversify supply chains. Continued US financial and diplomatic support is crucial to help these initiatives succeed and secure long-term supply chain resilience.

International partnerships also help close technological gaps in rare earth extraction and processing. Australia’s Critical Minerals Research and Development Hub coordinates global R&D efforts, while Japan’s Muroran Institute of Technology runs a dedicated rare earth research center. By leveraging these collaborations, the US can gradually strengthen its domestic capabilities and reduce vulnerability in a sector currently dominated by China.

(Also read: Trump vs. Taiwan: Who Will Win the Chip Battle)

China–US meeting: Key developments

In late October, Trump met Chinese President Xi Jinping at Busan airport in South Korea, highlighting a series of announcements aimed at easing trade tensions between the world’s two largest economies. The meeting capped Trump’s whirlwind Asia tour and delivered a partial de-escalation, including reduced tariffs on select Chinese imports to the US.

Beijing, for its part, signaled a softer stance by pausing the rare earth export controls it had unveiled earlier in the month. Trump said China also committed to purchasing what he described as ‘massive’ volumes of soybeans and other US farm goods. Still, despite the gestures, no formal agreement has been signed, and the two powers, after months of economic pressure tactics, remain without a binding deal.

Washington moved to halve a 20% tariff imposed to curb the flow of fentanyl, although overall duties on Chinese goods still hover just below 50%. According to statements from both sides, Trump and Xi used the meeting to tackle a broad agenda that spanned trade, Russia’s war in Ukraine, fentanyl trafficking, and the situation in Taiwan.

The US also withdrew its threat to impose an additional 100% tariff on Chinese products, while Beijing postponed the rollout of its latest round of rare earth export controls.

As one of the Top 20 EMS companies in the world, IMI has over 40 years of experience in providing electronics manufacturing and technology solutions.

We are ready to support your business on a global scale.

Our proven technical expertise, worldwide reach, and vast experience in high-growth and emerging markets make us the ideal global manufacturing solutions partner.

Let's work together to build our future today.

Other Blog